Freight fraud is a multi-billion-dollar problem, and the old verification model is broken. Here’s the new standard every broker needs to build toward in 2026.

S&P is cautiously optimistic about the freight recovery, but it still kept RXO's rating below investment grade. Plus: the Strait is set to reopen, Volvo pulls the safety driver, the U.S. goes after cheap trailers, and more.

The World Cup kicked off, and Amazon decided to become forklift certified. Plus: the Fed could spoil freight's party, C.H. Robinson in crosshairs again, the World Cup is a freight problem, and more.

How did a rather unimpressive coffee shop become one of the largest cargo insurers in the world?

If you've worked in freight, it's likely you've run across Lloyd's of London.

Lloyds of London did not start as one of the largest insurance companies in the world, but rather as an unimpressive coffee shop in London.

Today's Newsletter is Brought to You By OTR Solutions.

Edward Lloyd had a coffee shop called Lloyd's Coffee Shop near the docks in London. The cafe was known not for its coffee but for its location.

His Regulators were shipowners, merchants, and captains who came to discuss developments in the freight world.

In the late 17th century, those ship owners had one specific problem. Pirates.

The Atlantic shipping lanes were filled with pirates, and owners were losing merchandise left and right.

After months of eavesdropping, he knew which captains he could trust and which ships were seaworthy.

Lloyds's coffee shop became one of the most important rooms in the world. Merchants and investors began making deals with each other to insure each other's shipments.

They would draft an agreement for a sum of money to cover the cost of goods lost or stolen. They would sign their name at the BOTTOM of the agreements.

"Post and Pray" shouldn't be the only way to find new capacity - and now with OTR Select, it's never been easier to find reliable capacity and market insights.

Real Capacity: Built on millions of invoice-backed loads from continuously vetted carriers, not self-reported or scraped data.

Real Rates: View legitimate lane rates based on what carriers are actually accepting, helping you quote faster and protect margin.

The Most Secure Network: Every carrier in the OTR Network is vetted on entry and continuously monitored 24/7/365.

OTR Select is a capacity and rate intelligence platform now available to a select group of vetted brokers.

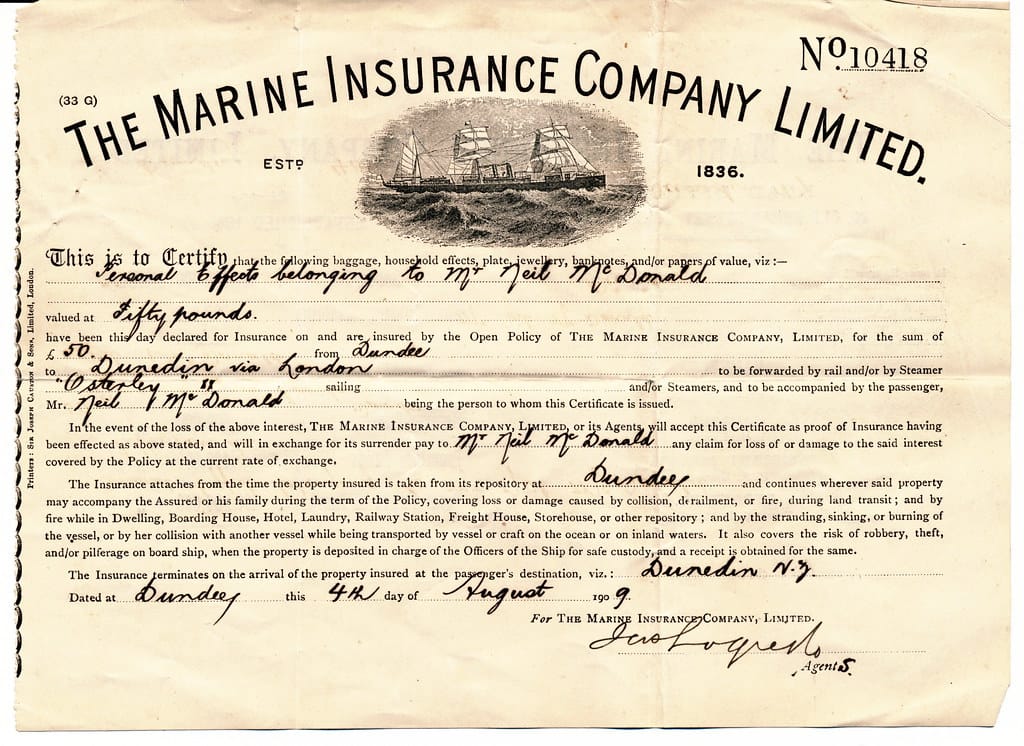

Marine insurance certificate from The Marine Insurance Company Limited (est. 1836). Not affiliated with Lloyd’s, but built on the same underwriting model Lloyd’s pioneered for insuring cargo at sea. Image Source: Flickr.

Edward Lloyd didn't set out to build the global insurance market. He just had a good location and a knack for useful information. But that forgettable coffee shop became Lloyd's of London, and Lloyd's of London became one of the largest cargo insurers in the world.

Over the next century, Lloyd's formalized. The guys signing policies organized into syndicate groups, pooling capital together to share risk (also known as "Names." Brokers would bring a risky shipment to the floor, syndicates would quote a price, and everyone would go home hoping for calm seas.

By the 1800s, Lloyd's was insuring the cargo that moved empires. Cotton, spices, timber. If it floated, Lloyd's priced it.

Then aviation showed up. Lloyd's was writing aviation policies before most people had ever been on a plane. Then, offshore oil rigs. Then satellites. Lloyd's basically has a policy of 'if it's weird, we'll quote it.

The 1980s and early 90s were a disaster. Asbestos liability claims. Hurricane Hugo. The Piper Alpha oil platform explosion. Hurricane Andrew. The losses stacked so fast that Names started getting letters saying they personally owed millions of pounds.

People lost homes. There were lawsuits. There were suicides. It was bad.

Lloyd's survived through a restructuring that ring-fenced all the toxic legacy losses and — for the first time — opened the market to corporate capital. The Names system still exists, but corporations can now back syndicates as well.

Lesson: Unlimited personal liability sounds fine until it doesn't.

Trinity Freight Agents benefit from clear commission structures, dependable pay cycles, and full visibility into earnings so you can focus on moving freight, not chasing checks.

The cargo insurance market your shippers ask about, the one you're probably not spending enough time selling, flows directly out of the Lloyd's model. Marine cargo insurance, inland transit, freight liability, specialty coverage for high-value or high-risk freight: Lloyd's either writes it directly or sets the benchmarks everyone else follows.

For freight brokers, here's the thing: cargo claims are where customer relationships go to die. When a shipper's load gets damaged, and there's no solid coverage in place, you're the first call.

Why do some brokerages not allow Lloyd's?

A few reasons,

The big one: Lloyds is non-admitted (surplus lines) in almost every U.S. state

Lloyd's is only a fully admitted insurer in one U.S. state — Kentucky. Everywhere else, it operates as a surplus lines carrier. The difference matters:

Admitted carriers are regulated by your state's insurance department and backed by state guaranty funds. If they go under, the state backstops your claim.

Surplus lines carriers like Lloyd's are less regulated and have no state guaranty fund protection. If something goes sideways with the syndicate, you're not protected the same way.

Some 3PLs have contracts — especially with larger shippers or in certain industries — that specifically require admitted carrier coverage. Lloyds simply can't satisfy that requirement in most states.

The claims process is more complex

Lloyd's isn't one company. It's a market of syndicates, and a single policy might be spread across several of them. When a claim hits, it can involve multiple parties, which can slow things down and create friction that a 3PL with a big shipper relationship doesn't want to deal with.

Risk perception (fair or not)

Some procurement and legal teams at shippers see "Lloyd's of London" and flag it as foreign, non-standard, or unfamiliar. Even if the coverage is solid, getting it through a corporate insurance compliance checklist can be harder than a domestic admitted carrier — and 3PLs operating under those shipper contracts have to comply.

The irony

Lloyd's literally invented cargo insurance. But the regulatory patchwork of the U.S. insurance market means the most sophisticated specialty insurer on the planet sometimes can't get through a shipper's vendor approval form. Very freight industry.

Freight fraud is a multi-billion-dollar problem, and the old verification model is broken. Here’s the new standard every broker needs to build toward in 2026.

S&P is cautiously optimistic about the freight recovery, but it still kept RXO's rating below investment grade. Plus: the Strait is set to reopen, Volvo pulls the safety driver, the U.S. goes after cheap trailers, and more.

The World Cup kicked off, and Amazon decided to become forklift certified. Plus: the Fed could spoil freight's party, C.H. Robinson in crosshairs again, the World Cup is a freight problem, and more.

Keep up with the freight broker world in 5 minutes.

Join over 14K+ subscribers to get the latest freight news and entertainment directly in your inbox for free. Subscribe & be sure to check your inbox to confirm (and your spam folder just in case).