Newsletters

🎣 Chicago Takes the Crown

Plus: Brokers return, Hormuz spikes rates, LTL stays stuck in a tough year, and more.

Plus: Brokers return, Hormuz spikes rates, LTL stays stuck in a tough year, and more.

“If you can build it, own it, and it works as well as what you’re paying for—why wouldn’t you?”

Diesel is climbing, produce lanes are tightening across the board, and brokers on Reddit are fantasizing about quitting. Here is what's trending this week on X, LinkedIn, Reddit, and YouTube.

A high commission split means nothing without stability. Learn how credit exposure, factoring risk, and financial discipline impact freight agent income and why the right agency foundation matters most.

Most agents ask the same first question: “What’s the commission split?”

It makes sense. If you’re building a book of business, grinding for every load, every margin dollar, you want to know what percentage you keep.

But here’s the truth: Your split doesn’t matter if the agency behind you isn’t stable.

In an independent model, you’re not just plugging into a logo. You’re plugging into someone else’s financial decisions.

If that agency mismanages cash flow…

If their credit reputation slips…

If a major shipper defaults and they weren’t insured…

If a factor tightens limits overnight…

It won’t show up in the marketing brochure. It will show up in your commissions.

Not selling isn't the key issue. Agents fail because they underestimate risk.

“We pay on time” is the bare minimum. Financial stability requires control of cash flow, credit exposure, collections, and risk when the market turns.

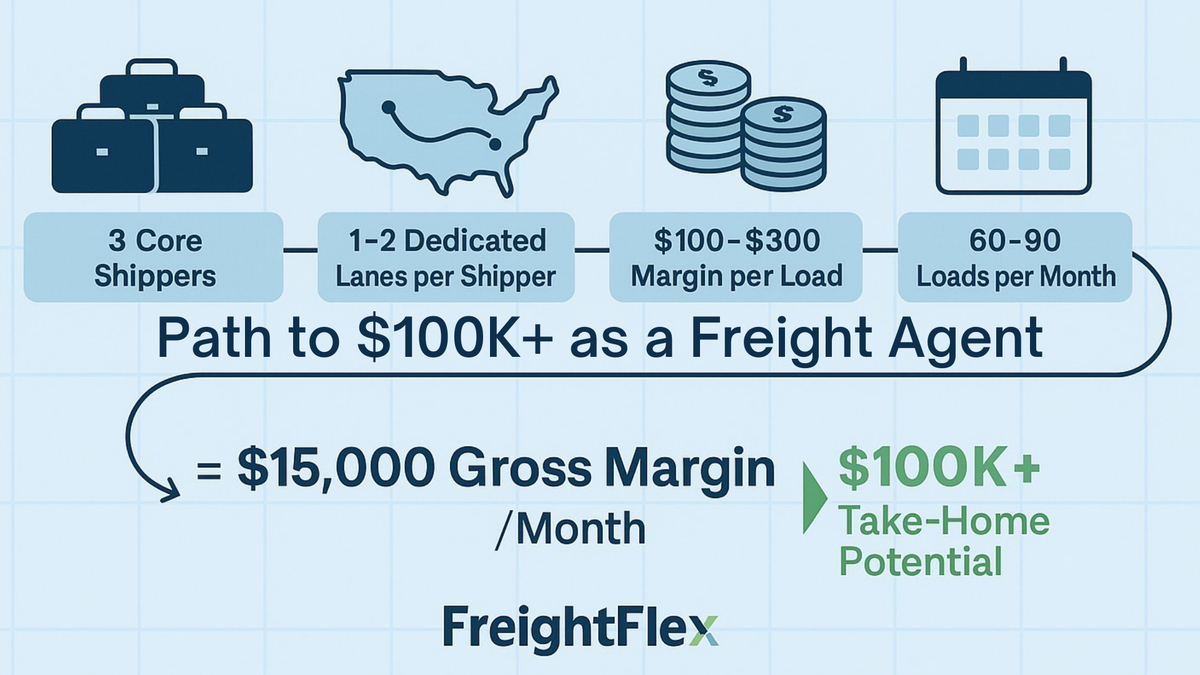

When you build a $15,000-a-month gross margin book, you’re building a real income stream. So the real question isn’t just how much of that you keep, but who’s protecting it.

That’s the first thing serious broker agents should be asking.

Here’s something many agents overlook: An agency’s financial health lives outside its walls.

It lives with:

If carriers hesitate to haul your loads, it’s mainly a credit issue. If factoring companies restrict exposure, that’s related to the brokerage’s standing.

Some agencies struggle quietly with acarrier acceptance or collections friction. Loags get harder to cover, dispatch becomes tense, and trust erodes. And the agent feels it first.

A strong external credit profile creates:

You can’t build a premium book of business on shaky credit reputation.

There are two risks agents cannot control:

If an agent doesn’t manage exposure properly – or worse, isn’t protected – one major default can destabilize everything. That’s where disciplined credit management and credit insurance matter.

Credit insurance isn’t just a corporate tool, but a shield for agents. It prevents catastrophic write-offs, caps exposure, and ensures one bad shipper doesn’t wipe out months of work.

It also protects agents from overextending themselves.

Sometimes growth feels exciting. One shipper becomes half your book with strong margins and steady volumes.

But concentration risk is real.

A financially disciplined agency manages exposure limits to protect sustainability.

That’s the difference between scaling income and gambling it.

Here’s another uncomfortable conversation most agents never have: Who actually controls the money?

Many agencies rely heavily on factoring. On the surface, it seems simple enough. You get fast cash and smooth flow. But factoring comes with strings attached.

Factors wield a lot of control. They:

So what does that mean? It means an outside party can indirectly control your growth. It may begin as short-term relief, but over time, it creates dependency. When your agency’s liquidity depends on a third party, it leaves you operating from borrowed stability.

No Factoring. No Private Equity. Full Control.

A self-funded model changes the equation. When an agency controls its own capital:

What does stability look like? How do you know what to look for?

Stability is quiet; it looks like operational maturity, risk management discipline, and long-term thinking.

When you build a $15,000 monthly gross margin book, you’re building a six-figure income engine.

At $19,000 monthly GM, you’re approaching $125,000 take-home. At $23,000, you’re pushing toward $150,000.

That is real income. But income without protection is fragile. The wrong agency partner won’t just cap your upside, but they can also expose you to unnecessary downside. And downsides in this business can move fast.

Yes, commission splits are important, but they’re second place. The first question serious agents should ask is:

Focus on stability, because the strongest commission structure in the world means nothing if the platform behind it can’t weather the storm.

Freight Flex is self-funded, credit-insured, and built for long-term resilience.

No factoring. No external capital pressure. No hidden risk layers.

If you’re serious about protecting yourincome stream, start here:

👉 Connect with Freight Flex to explore the agency model.

Stop babysitting freight. See how Kingsgate Logistics uses Chain AI to automate 93% of carrier messages and scale operational judgment.

Most freight AI pilots work. Most enterprise rollouts don't. Here's what's actually breaking down and what production-grade AI infrastructure looks like in freight.

B1 visa drivers and illegal operators are not the same thing. Here's the difference and why conflating them is hurting the industry.

Freight margins are razor-thin. The brokerages surviving it built nearshore teams that actually work.

Join over 14K+ subscribers to get the latest freight news and entertainment directly in your inbox for free. Subscribe & be sure to check your inbox to confirm (and your spam folder just in case).